New York City’s new pied-à-terre surcharge, commonly described as a pied-à-terre tax, took effect July 1, although some details of its administration remain subject to proposed Department of Finance rules. Most of the attention has focused on the obvious questions: who gets hit, how much, and which properties fall into scope.

Those are fair questions.

But beneath all of them is a more difficult one, and for many owners, attorneys, brokers, and advisors, it may turn out to be the most important one of all:

How will market value actually be determined, supported, and defended?

That is where this stops being just a tax story and starts becoming a pricing story.

The real issue is not the tax. It is valuation.

But the value used by the surcharge will change over time. During the initial two-year phase, potential exposure for condos is based on the Department of Finance’s existing “estimated market value” for the unit. For co-ops, the building’s estimated market value is allocated among apartments according to their shares. Beginning in 2028, the City is expected to transition toward a new valuation system informed by comparable condo and co-op sales, although the final methodology has not yet been fully established.

When surcharge exposure depends on a government-assigned property value, the conversation shifts toward how that value was calculated, how it compares with the apartment’s likely sale value, and whether the difference warrants further review.

Not broad opinions.

Not rough estimates.

Not generic comps pulled from a portal.

Actual, supportable market evidence.

And in NYC residential real estate, that is rarely as straightforward as it sounds.

Two apartments in the same building can trade at meaningfully different prices because of floor, view, layout, condition, renovation quality, outdoor space, timing, or simply the circumstances of the sale. That is not market inefficiency. That is the market.

The issue is not whether a property has a likely sale value. It does.

The issue is that the value assigned through the tax system may not match what that particular property would actually command in the market.

Why market value is not a clean number in NYC

In more liquid markets, “mark-to-market” sounds simple. You look at where comparable assets are trading and you infer a reasonable value.

Luxury NYC residential real estate does not work that neatly.

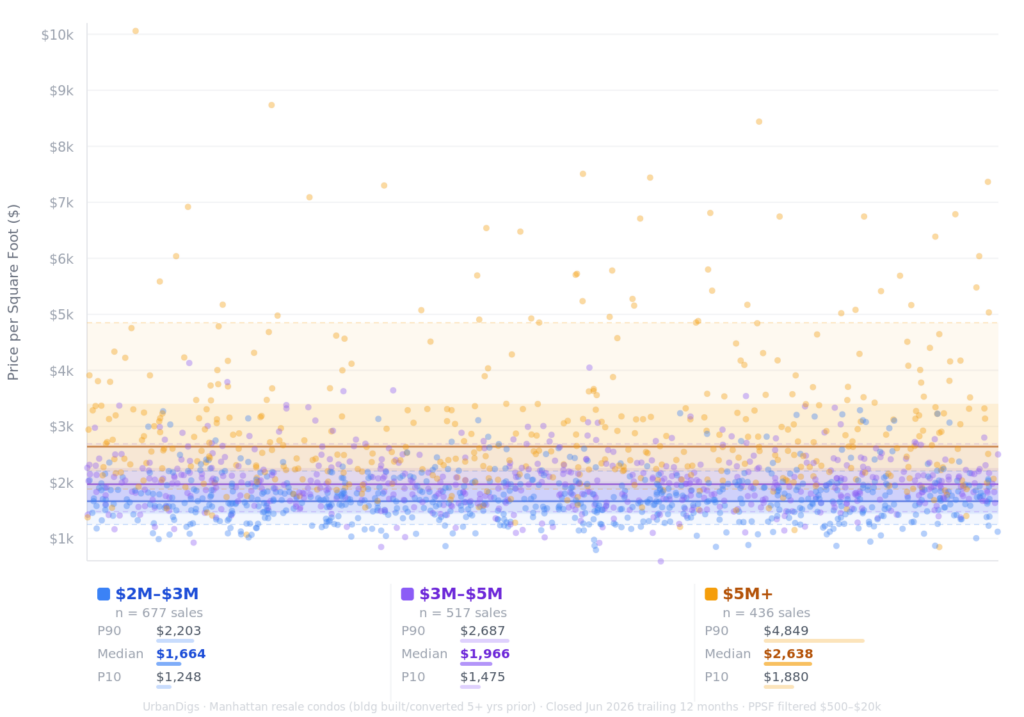

The current Phase One calculation begins with DOF’s tax-assessment values, not directly with observed sale prices. But actual transactions reveal how difficult it can be to determine whether an assigned value accurately reflects an individual apartment. Over the past 12 months, 1,318 Manhattan resale condos traded at $2 million or more. Within the $5M+ segment, price per square foot ranged from $1,914 at the 10th percentile to $4,782 at the 90th percentile. That is a spread of $2,869 per square foot within the same broad tier.

That kind of spread makes one thing clear:

Price tier alone does not tell you what a specific property is worth.

Key takeaway: even within the same tier, value dispersion is enormous. In the $5M+ segment, the spread between the 10th and 90th percentile is nearly $2,900 per square foot.

Data source: UrbanDigs, Manhattan resale condos, July 2025 to June 2026.

The comps problem

This is where the valuation issue gets harder.

Comparing a tax-assessment value with likely market value often requires comparable-sales analysis. That may sound precise, but in practice it demands judgment at every step:

- What is the right time window?

- Which sales are actually comparable?

- How should renovations be treated?

- How much should a view matter?

- What about outdoor space?

- What if one unit sold quickly in a multiple-offer setting and another sat for months before accepting a discount?

Those are not technical footnotes. They are the difference between a supportable valuation and a weak one.

The point is not that comps are useless.

The point is that in NYC residential real estate, comps are not self-executing. They need interpretation.

That is especially true when an administrative value can determine whether an apartment crosses a surcharge threshold and how much financial exposure follows.

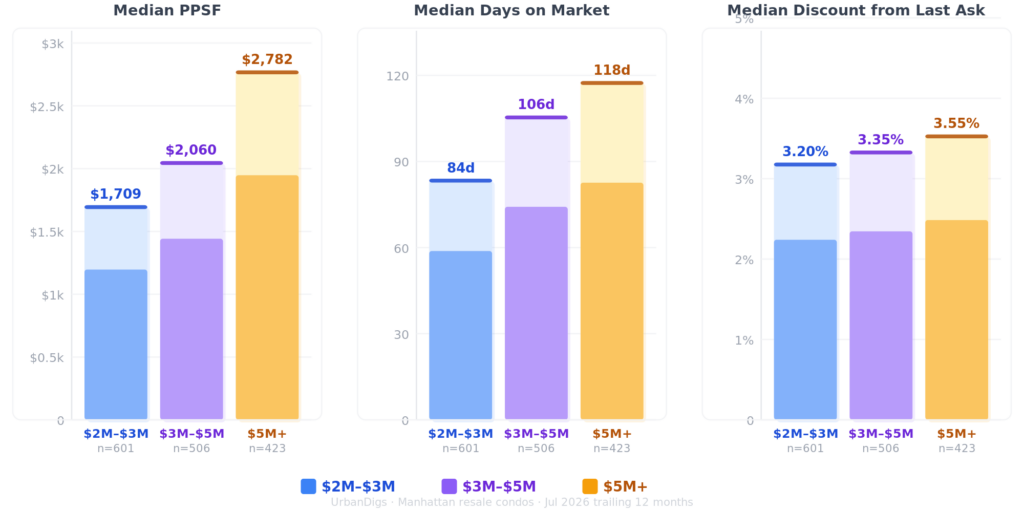

Key takeaway: outcomes vary meaningfully even within the same price band. Value is not just a function of category. It is a function of specifics.

Data source: UrbanDigs, Manhattan resale condos, July 2025 to June 2026.

Why this matters for agents, attorneys, and advisors

The pied-à-terre surcharge may affect a relatively narrow slice of the market, but the questions it creates are highly relevant to the professionals who advise that slice.

Luxury agents are going to get questions from owners.

Attorneys may need independent market support to assess how a DOF value compares with the property’s likely sale value and whether the difference merits closer evaluation by the owner’s legal and tax advisors.

Advisors and family offices will want more than a casual pricing opinion if annual surcharge exposure is tied to an assigned property value.

That is where the problem shifts from policy to process.

The practical question becomes:

How was the value calculated, how does it compare with the apartment’s likely sale value, and what market evidence explains the difference?

That is not a legal question alone.

It is also a pricing and documentation question.

How UrbanDigs Can Help

UrbanDigs is New York City’s independent real estate pricing intelligence platform, built for situations where market value needs to be supported, not guessed at.

This is not legal or tax advice.

It is independent pricing intelligence grounded in:

- comparable sales analysis

- building-level context

- neighborhood market evidence

- supportable pricing ranges

- rental context where relevant

- documentation that helps explain where a property is likely to trade

For owners, attorneys, brokers, fiduciaries, family offices, and other advisors dealing with the new pied-à-terre surcharge, UrbanDigs can provide independent market evidence to help them understand, document, or evaluate a valuation position.

UrbanDigs Pricing Reports can support:

- independent market value analyses

- comparable sales packages

- comparable rental analysis

- building and neighborhood market studies

- valuation review in connection with professional advice, a potential challenge, or a sale decision

- documentation supporting a pricing position

- ongoing monitoring of competitive inventory and market conditions

When financial exposure depends on an assigned property value, broad estimates and generic comps are not enough. The analysis needs to reflect the property, the building, the neighborhood, and the market conditions shaping value today.

The takeaway

The pied-à-terre surcharge may be framed as a tax issue.

But for many of the people dealing with it, the harder problem will be valuation.

In Phase One, one important valuation question is how DOF’s tax-assessment value compares with the apartment’s likely sale value. In Phase Two, the challenge becomes how the City will use comparable sales to assign values across thousands of highly individual properties.

When a government-assigned property value becomes the basis for real financial exposure, the conversation changes. It is no longer enough to have a rough sense of price. You need supportable market evidence and a defensible view of where a property is actually likely to trade.

That is exactly where independent pricing intelligence becomes more valuable.

Have a client who may be affected?

UrbanDigs can compare the property’s DOF-assigned value with current market evidence and help identify whether the difference merits closer evaluation with the owner’s qualified legal and tax advisors.

👉 Schedule a Complimentary Property Value Review

Price is reality. Everything else has to prove it.

John Walkup is Co-Founder of UrbanDigs, the leading NYC real estate pricing intelligence platform. This article does not constitute legal or tax advice. Readers should consult qualified legal and tax counsel regarding their specific situation.

Data notes

- All sales data: Manhattan resale condos, July 2025 to June 2026

- DOM filter: 0 to 730 days

- PPSF filter: square footage greater than or equal to 300

- Source: UrbanDigs transaction database